Over 31 billion hryvnia in revenue: how the EVA chain doubled its revenue during the war – and what does Cyprus have to do with it

15 May 19:00 ANALYSIS FROM

ANALYSIS FROM

The EVA chain, operated by RUSH LLC, increased its revenue to nearly 32 billion hryvnia, effectively doubling its revenue over the four years of the war. The company ended 2025 with record financial results. At the same time, a Cypriot holding company appeared in the retailer’s ownership structure. This is evidenced by data from OpenDataBot, reports "Komersant Ukrainian". How the company managed to increase its revenue and why a successful Ukrainian business needs an owner in Nicosia right now—read on.

What are EVA’s revenues?

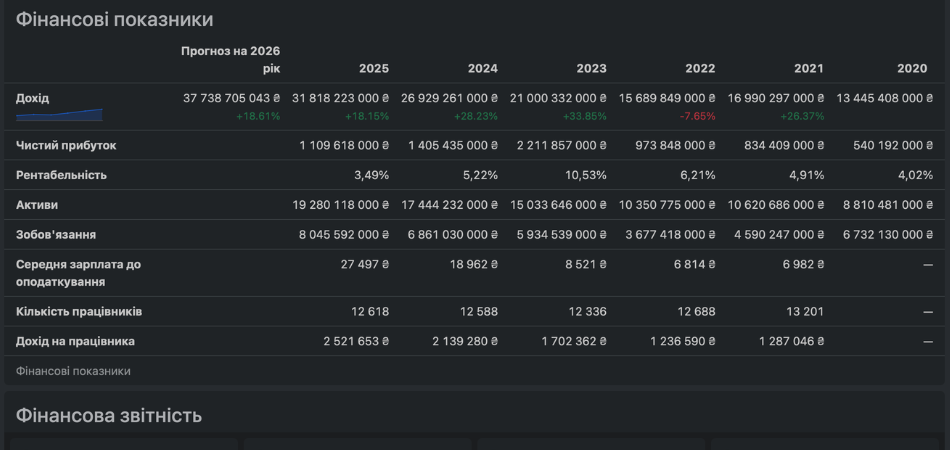

According to the company’s financial statements, RUSH LLC has effectively doubled its revenue during the years of the war. While in 2022—which was the toughest year for retail due to logistical shocks and the loss of territories—the company’s revenue stood at 15.6 billion UAH, by the end of 2025 this figure had risen to 31.8 billion UAH.

Overall, the company’s revenue grew 2.03-fold over three years, indicating adaptation to inflationary pressures, a shift in product mix, and likely a market realignment following the exit or weakening of competitors.

Watch us on YouTube: important topics – without censorship

However, profitability shows a different trend: after an abnormal peak in 2023 (UAH 2.2 billion in net profit), it fell to UAH 1.1 billion in 2025, which may be linked to rising operating costs, logistics, and the tax burden. The company plans to increase revenue to UAH 37.7 billion in 2026.

Cyprus “registration”

Against the backdrop of financial records, changes in the ownership structure are drawing particular attention. In August 2025 (according to registry data), the list of beneficiaries officially expanded to include a Cypriot entity. Although well-known Ukrainian businessmen Ruslan Shostak and Valery Kiptik remain the ultimate owners, the emergence of INSETERA HOLDINGS LIMITED (Nicosia, Cyprus) as the 100% owner of the authorized capital of RUSH LLC is a significant signal.

Economist Danilo Monin, commenting on such strategies for "Komersant Ukrainian", notes that Cyprus tax residency status for owners of large businesses is a preemptive move.

“Currently, the NBU restricts the payment of dividends abroad. However, having a Cypriot holding company creates a legal ‘gateway’ for future profit transfers. When the restrictions are eased, dividends from the Ukrainian ‘subsidiary’ can be transferred to Cyprus, where foreign owners are effectively not taxed,” explains Danilo Monin.

Tax Residency: The Two-Country Trap

The first and main problem faced by a business owner living in Cyprus is determining tax residency status. Formally, staying in the country for more than 183 days makes a person a resident. However, Ukrainian legislation has its own arguments.

“The law is worded in such a way that Ukraine can continue to consider the owner a tax resident, citing the ‘center of vital interests’ as grounds. For example, the ownership of real estate in Ukraine,” notes Danylo Monin.

As a result, there is a risk of double taxation, where both countries demand tax payments on the same income. Although a Double Taxation Convention is in effect between Ukraine and Cyprus, formally resolving this issue in practice remains a complex process.

Taxes and the military levy

If a Ukrainian company decides to pay dividends, it must pay corporate income tax, and subsequently, personal income tax.

“Most likely, they [the dividends] can be paid into the founder’s bank account opened in Ukraine. This occurs after the company itself has paid income tax. For an individual, the tax burden currently consists of 5% personal income tax and 5% military levy. After that, the owner can likely, subject to certain NBU restrictions, spend this money directly from the card or via transfer, although there are limits—apparently up to 50–100 thousand hryvnias per month,” explains Monin

As for Cyprus, this jurisdiction typically does not tax dividends received by foreign owners from abroad if the ownership structure is set up correctly. However, to take advantage of the benefits of the Cypriot system, the funds must first leave Ukraine.

Thus, having a Cypriot co-owner in the company’s structure today is not so much a “loophole” for quick tax savings as it is an attempt to lay the groundwork for future capital outflows. However, the combination of strict monitoring by the NBU and the risk of dual residency makes this strategy costly and legally precarious. The most reliable, albeit limited, method remains the payment of dividends in Ukraine followed by the use of funds through Ukrainian banking instruments.

Read us on Telegram: important topics – without censorship